The number of new seed investments on Carta declined 27% in 2023 compared to the previous year. Early-stage venture capital investors agree that this decrease in deals is not due to a change in supply. There are just as many promising young startups today as there were last year.

Instead, VCs say the dealmaking slowdown is due to a shift in demand. Early-stage investors have grown more selective. They’ve become more focused on tangible metrics like revenue and profitability and less likely to be swayed by growth metrics alone.

Julia Gudish Krieger has watched this evolution unfold from her perch as managing partner at Pari Passu Venture Partners, an early-stage firm focused on the SaaS and commerce enablement sectors. She says the change has been particularly interesting at the seed stage.

How the seed scene has shifted

Earlier in 2023, Krieger says many seed startups that were seeking capital in a difficult market ended up raising down rounds. This tracks with the data: More than 19% of all new investments on Carta throughout 2023 came at a lower valuation than the previous round, the highest annual rate of down rounds since at least 2017. But as the year progressed, Krieger noticed a growing number of promising seed startups taking a different path. For young startups with impressive early metrics—but perhaps not quite impressive enough to raise their desired Series A—she saw a trend away from raising new primary rounds and toward raising seed extension rounds.

These extension rounds and other types of bridge rounds have allowed companies to extend their runways while waiting for friendlier market conditions to complete a full-fledged round of new primary funding.

Download bridge round data by sector“There’s a little bit of a shift there,” Krieger says. “Companies that had significant growth in the last 12 months but had raised at those heightened valuations (in 2021 and early 2022) are not doing down rounds. They’re doing seed extensions.”

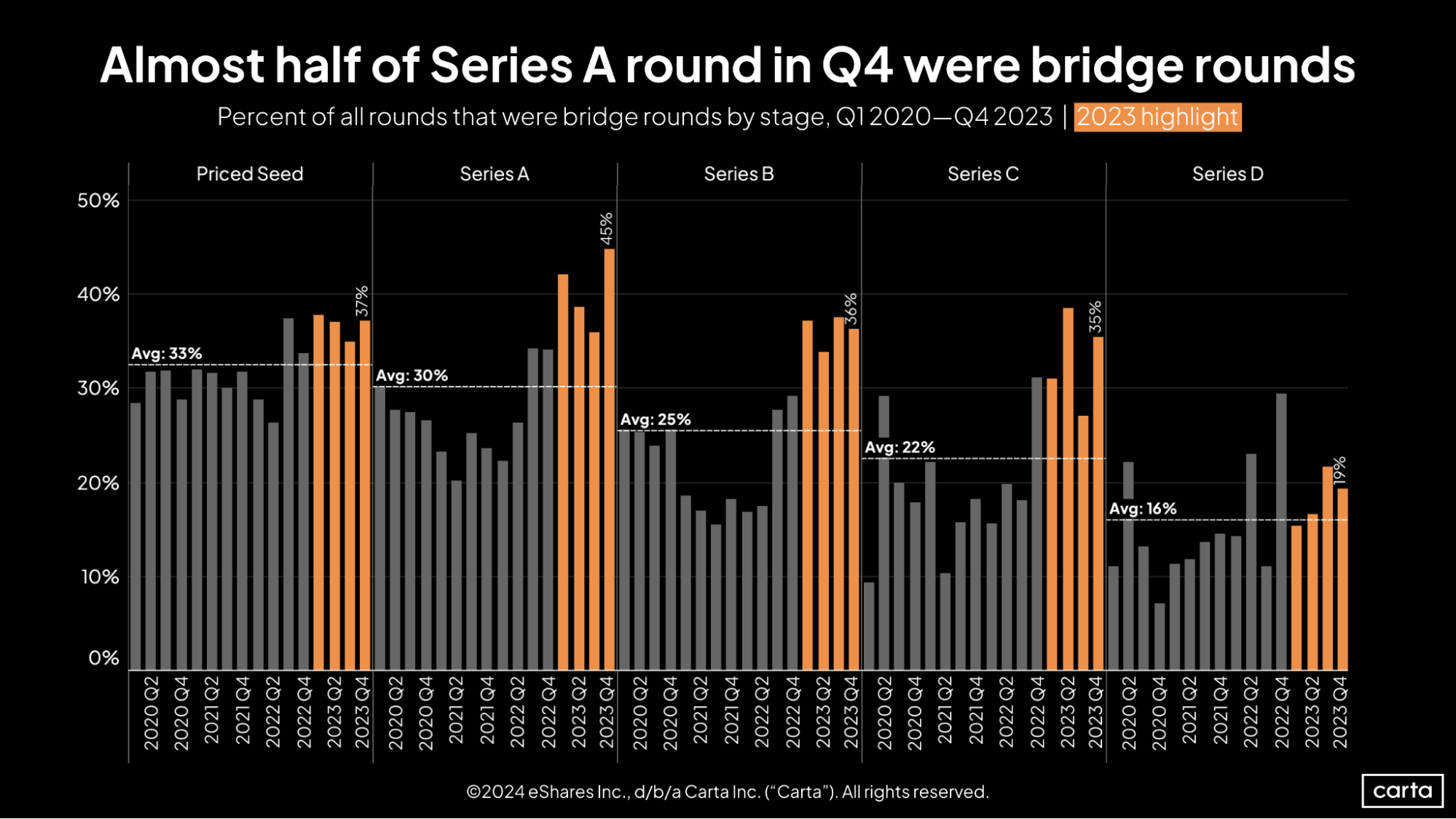

Bridge rounds are on the rise

This trend isn’t isolated to seed startups. At every stage of the startup lifecycle, the frequency of bridge rounds increased significantly in 2023.

The rate of bridge rounds among Series A startups hit 45% during Q4, the highest figure for any stage in any quarter so far this decade. Every other startup stage also established a quarterly high for the rate of bridge rounds at some point in 2023, with the exception of Series D, which peaked in Q4 2022.

At later startup stages, a bridge round typically comes after a priced funding round. That’s not always the case at seed. In many cases, Krieger says that the company’s latest round was structured as a SAFE, rather than a priced equity round. An extension to that SAFE might look different than an extension to a priced seed round, in terms of the implications for the cap table and the impact on investors’ holdings.

New attitudes toward bridge rounds

Historically, investors and founders have viewed extensions and other types of bridge rounds with some skepticism. Bridge rounds were relatively infrequent during the extended bull market of the 2010s and early 2020s. When raising a new primary round at an attractive valuation was so easy, the thinking went, why would a startup raise an extension instead?

Krieger says that calculus has changed amid the current venture landscape. Deal counts and valuations have both declined at nearly every startup stage. In this environment, the attitude toward extension rounds is different.

“Companies that are raising seed extensions, and sizable seed extensions, are actually getting positive optics around it, versus anyone focusing on the valuation,” Krieger says. “That’s been something that’s interesting to watch.”

Building longer bridges

In addition to the increase in seed extensions and other types of bridge rounds, Krieger says she’s seen these extensions grow larger. In an uncertain market where fewer deals are getting done, some founders are prioritizing the size of a check over other factors, such as valuation.

No matter what type of round a startup might be raising, Krieger thinks it makes sense for founders to try to stretch their runways as long as possible.

"Don’t worry about getting cute on valuation,” Krieger says. “Focus on bringing in real runway and excellent partners who can help you weather any storms ahead.”

Bridge round data by sector

Download the addendum for additional data on bridge round frequency by sector.